The Steel Dilemma: A Path Towards Decarbonization

The journey to decarbonization is fraught with challenges, and one of the most significant problems arises from the steel industry . For every ton of steel produced, approximately two tons of CO₂ are emitted into the atmosphere. While research is ongoing to explore more sustainable alternatives , steel remains indispensable, especially in regions where megaconstruction projects are on the rise. The world’s leading supplier of steel is none other than China , a country that dominates this crucial sector.

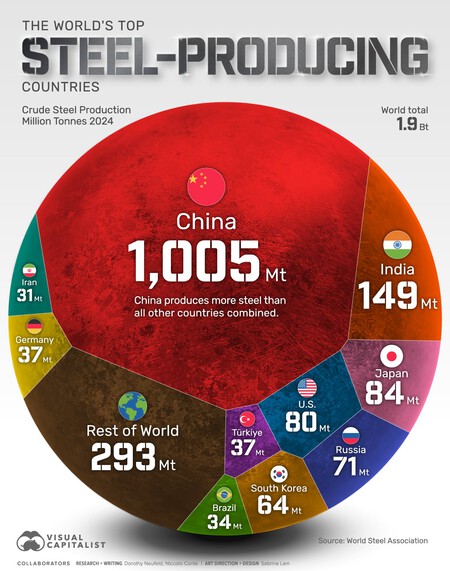

This reality is starkly illustrated in a graph by Visual Capitalist:

China’s Dominance. According to the World Steel Association, in 2024, global steel production is estimated at approximately 1,884.6 million tons , with more than half produced by China . The gap between Chinese production and that of other nations is staggering, with India’s Tata Steel Group being one of the few notable exceptions that have benefitted from increased infrastructure investment. Other producers are struggling to keep pace.

China’s ascendance in the steel industry is no accident. Following the foundation of the People’s Republic in 1949, the state deemed steel production crucial for industrialization. The domestic demand for steel surged due to a robust manufacturing sector and construction boom. Although China also exports steel, the focus remains on meeting its own monumental consumption needs.While exports are significant, domestic consumption remains paramount.

The U.S. Response. This overwhelming dominance poses a challenge for other countries, as the U.S. has become increasingly concerned about its dependency on China’s steel production. The United States , historically a major player in the steel sector, is intent on reclaiming its industrial territory. Recently, U.S. Steel , one of the oldest steel manufacturers, nearly fell into the hands of the Japanese conglomerate Nippon Steel . However, President Biden intervened, blocking the acquisition citing national security, sending a clear message about the importance of protecting American interests.

Europe’s Challenges. In Europe, Germany holds the title as a steel powerhouse, but even this giant is facing challenges. Reports from The New York Times reveal that German steel production has dropped by 11.6% in the first half of 2025. Despite having advanced technology in facilities like Tata Steel in the Netherlands, strict environmental regulations, Chinese dumping , and tariff policies are sidelining Europe in the global steel market.

Spain’s production mirrors this trend, with an estimate of 11.9 million tons in 2024, reflecting a 3.7% increase over the previous year. However, demand still outpaces production capabilities, amplifying the pressure to reduce emissions and limit imports, particularly from Asian steel producers.

Environmental Constraints and Overproduction. Interestingly, despite the ongoing hunger for steel globally, producers are facing an overproduction crisis . According to the OECD , excess world capacity could reach 721 million tons by 2027. China is recognizing this issue and has started to implement measures to regulate its production capacity effectively. Initiatives such as allowing firms to produce only under firm orders or stalling expansions aim to curb overcapacity, a decision that reflects both local and global consequences given China’s sheer market presence.

These measures aim to prevent a crisis where low prices threaten the sustainability of their steel industry. While seemingly localized, any action taken by China is bound to resonate across the global marketplace, affecting steel prices and availability worldwide. In a landscape where demand continues to surge, the imbalance between supply and environmental considerations poses complex questions for the future of this vital industry.