Nvidia has recently released its financial results for the second fiscal quarter, showcasing impressive figures that technically surpassed forecasts:

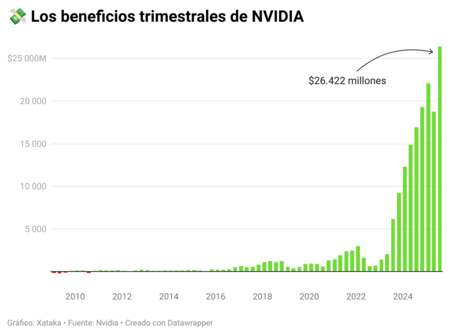

- Adjusted earnings of $1.05 per share compared to the expected $1.01.

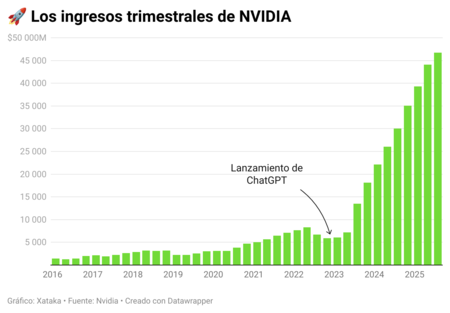

- Revenues reached $46.74 billion, beating the anticipated $46.23 billion.

The company also provided a forecast of $54 billion for the current quarter, slightly above the consensus estimate of $53.4 billion.

Why is this significant? These strong numbers have not satisfied a market eagerly watching Nvidia as the benchmark for the ongoing AI boom .

Indeed, the stock has plummeted by 3% in after-hours trading, reflecting the immense pressure on one of the world’s most valuable companies, currently valued at a whopping $4.4 trillion. The expectations have reached almost unattainable levels.

The China Factor. One significant drawback in these results has been the complete absence of sales for the H20 chip in China during the quarter. Nvidia has not included any sales forecast to the Chinese market in its guidance for the third quarter. Despite this, the company’s Chief Financial Officer, Colette Kress, indicated that they have between $2 billion and $5 billion in ready-to-ship orders dependent on geopolitical circumstances.

Nvidia is currently waiting for clarification from the Trump administration regarding the proposed 15% restrictions on chip sales to China.

During the analyst call, CEO Jensen Huang was unusually candid: “The Chinese market represents approximately $50 billion of opportunity for us this year.”

- He noted that half of the world’s researchers are based in China.

- Huang emphasized that it is “quite important” for American tech firms to access the Chinese market.

Reading Between the Lines. Huang’s frustration with the current geopolitical landscape is evident. His comment on the need to “continue advocating” before the Trump administration suggests that negotiations may be more tense than what official statements portray.

The CEO also mentioned that they are developing a modified version of their Blackwell chips for the Chinese market, which would have reduced performance . This indicates Nvidia’s willingness to compromise to retain access to this lucrative market, a noteworthy move for such a formidable company.

Data Center Dilemma. The data centers segment , which contributes 88% of Nvidia’s total revenue, generated $41.1 billion, slightly missing expectations of $41.29 billion.

This marks the second consecutive quarter of underperformance for this critical segment, raising concerns as major tech players like Google and Microsoft invest substantial amounts into AI infrastructure each quarter.

“Everything is Sold”. Huang stated that “everything is sold,” referring to both the current Hopper chips and the upcoming Blackwell chips. He also reassured stakeholders that the production of Blackwell Ultra is progressing and that the demand is “extraordinary.”

However, these statements stand in contrast to the fact that the year-on-year income growth of 56% is the slowest in nine quarters of over 50% growth.

Rising Pressure. The market’s reaction reveals a troubling reality: Nvidia has become a hostage to its own remarkable success . Currently, the company’s weight in the S&P 500 is approximately 7.5% , up from 3% last December. Any potential setbacks can significantly impact the entire market.

A major shortfall from Nvidia could trigger a downturn in global stock markets.

Contrasting Promises. Huang projected that AI infrastructure spending will amount to between $3 billion and $4 billion by the end of the decade. However, immediate circumstances show that Nvidia is hindered in its ability to access the world’s second-largest computing market.

The $60 billion share buyback authorized by the board—one of the largest in American corporate history—appears more as an effort to support stock prices rather than a genuine confidence signal regarding future performance amidst regulatory uncertainties.

Nvidia’s future hinges on navigating these complex challenges, from geopolitical tensions to sustaining its impressive growth rate. How it adapts to these hurdles will determine its trajectory in the evolving tech landscape.