Telefónica’s Departure: A Reflection on Mexico’s Telecom Landscape

The recent sale of Movistar Mexico to Melisa Acquisition for $450 million marks the end of over two decades of Telefónica’s operations in Mexico. Despite investing more than €3.6 billion, the Spanish operator faced a persistent struggle against a dominant market player, Telcel. This situation exposes the uncomfortable truth about Mexico’s telecommunications market: it lacks a viable alternative to Telcel.

Why Does It Matter?

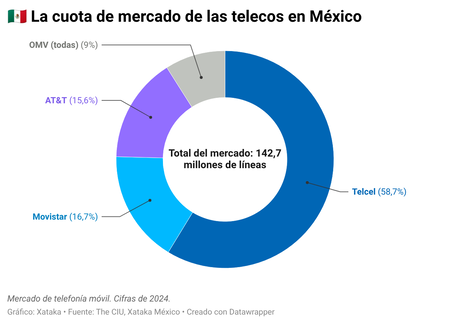

The departure of Telefónica would conventionally suggest a significant market shift, yet it reinforces a troubling reality. Mexico boasts one of the most concentrated mobile markets globally, with Telcel—owned by Carlos Slim—commanding nearly 60% market share. Competing firms have been unable to grow their market share sustainably throughout the 21st century. Notably, the length of Telefónica’s tenure in the country becomes puzzling when considered against the backdrop of its recent strategic retreat from Latin America.

Background: The Monopolistic Environment

Telcel’s dominance stems from its inheritance of Telmex’s extensive commercial infrastructure, customer base, and market muscle following its privatization in 1990. Regrettably, Mexican regulatory bodies have struggled, or perhaps lacked the will, to foster a balanced competitive environment since then.

The Role of AT&T

AT&T entered the Mexican scene with ambitions of its own, yet it remains below a 16% market share, indicating considerable challenges in penetrating Telcel’s dominance. In 2019, Telefónica was forced to return its spectrum, which left it minimally operational, reliant on AT&T’s infrastructure. Essentially, it became what is referred to as a “premium MVNO,” devoid of its own network and operational flexibility.

The New Entrants: Implications for Users

The new owners, Melisa Acquisition, composed of Oxio (a technology platform for virtual operators) and an investment fund, signify a shift in strategy. They aren’t looking to invest in robust network infrastructure or challenge Telcel; their goal is merely to manage the existing customer base while hoping to leverage technology for marginal profit improvements.

Financial Viability Concerns

The average revenue per user (ARPU) starkly illustrates Telefónica’s struggles: at just 64.7 pesos per monthly subscriber, it underperformed in comparison to AT&T (141.1 pesos) and Telcel (176 pesos). This scenario doesn’t just indicate a lack of clients; it reflects low profitability, unsupported by any substantial network investment. Thus, this sale isn’t a strategic retreat but rather the culmination of operating within a perpetually low-margin market.

What Lies Ahead for Mexican Users?

As Telefónica exits, the primary casualties are the Mexican consumers. With a weakened competitive landscape, Telcel’s grip on the market is further solidified. Effective competition in pricing, coverage, and services will now rely heavily on AT&T, which, as previously noted, has struggled to make inroads against Slim’s holdings.

Furthermore, Mexico will not only be down one operator but will also lose one of the few incumbents willing to innovate and push for better services.

Conclusion: A Call to Action

In light of these developments, it becomes imperative for Mexican regulators and policymakers to rethink their approach to the telecommunications sector. The need for competitive balance is greater than ever, as the absence of viable alternatives puts consumers at a disadvantage. A more diversified market would not only foster competition but also encourage innovation, ultimately benefiting the user base in Mexico.