If the question is which AI makes better images, the general answer would be Google’s Nano Banana 2. And if we talk about preparing reports rigorously, we would probably say that Claude is the one who takes the lead. But in the AI race, just as important as being the best is appearing to be the best. And, above all, making money with your model.

The Shift in AI Preferences Among Companies

With the arrival of artificial intelligence in the labor market, companies have witnessed a seismic shift, manifesting as layoffs, increased barriers for entry-level roles, and heightened competition for positions. Recently, the landscape of which AI is favored by companies has drastically changed.

Market Insights from Visual Capitalist

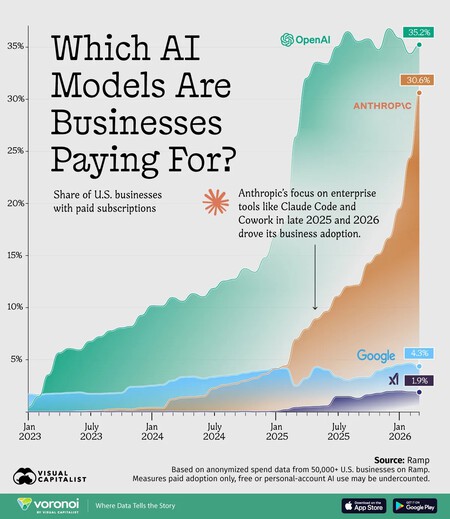

Visual Capitalist has published a graph that monitors spending by U.S. companies on various AI models from January 2023 to March 2026. This data, derived from over 50,000 companies via the platform Ramp, focuses solely on paid subscriptions, painting a clear picture of the market’s consolidation.

The graph identifies a clear winner: OpenAI, which commands a staggering 35.2% share of the market as of March this year. Close behind is Anthropic, with a notable 30.6%. Other players like Google and xAI are trailing significantly, each below 5%, but the upward trajectory of Anthropic is particularly striking.

Concentration of Market Share

The market appears increasingly precarious, with only room for two major players: OpenAI and Anthropic collectively account for about 66% of the AI payment market among U.S. businesses. Essentially, two out of every three dollars spent on AI models go to these two companies, while others are left to share the sparse leftovers. This concentration is a self-perpetuating cycle: leading companies gain more customers, accumulate data, and secure resources to enhance their offerings, creating formidable barriers for competitors. Although Google still has the technical strength, its market share reflects a troubling trend.

Key Data Points

January 2025 serves as a crucial inflection point in this landscape. At that time, OpenAI was integrated into 16.8% of companies while Anthropic barely registered at 4.1%, just shy of Google’s 4.2% share. Fast forward 14 months, Anthropic experienced a meteoric rise, multiplying its market presence sevenfold, while OpenAI grew by 100%, and Google only marginally improved to a 4.3% share. This growth aligns with Anthropic’s strategic product launches, including Claude Code and Cowork, which bolster its appeal to businesses.

The Rise of Anthropic

The rapid ascent of Claude is not solely due to its quality. Anthropic has skillfully developed practical tools that companies integrate into their daily operations, creating dependencies that complicate vendor switches. According to estimates from Sacra, Anthropic boasted over 300,000 business clients by October 2025, generating approximately 80% of its revenue from corporate partnerships—signifying a focused strategy on enterprise solutions rather than individual users.

Google’s Disappointing Performance

In stark contrast, Google’s market presence has fluctuated between 3% and 4.5% over the past three years—a marginal increase compared to the emerging duopoly despite substantial investment. Elon Musk’s xAI has progressed from zero to 1.9% by March 2026, finally breaking into the competitive picture but still remaining far behind the leaders. The perplexing case of Google underscores the issue: despite pioneering technology, robust cloud infrastructure, and an abundance of data, it struggles to convert companies into paying clients. The likely culprit is a confusing array of bundled products across various platforms, leading to ambiguity and indecision among business customers.

In conclusion, while the AI landscape remains dynamic, the recent trends indicate a growing dichotomy where only a couple of players may thrive, leaving others either significantly behind or struggling to catch up.