Shifting Trade Dynamics: The EU’s Historic Commercial Surplus with Russia

The European Union recently marked a significant turning point in its trade relationship with Russia, achieving a commercial surplus for the first time in years. In the second quarter of 2025, the EU reported a positive balance of 500 million euros with Moscow, a notable shift from a substantial 47.4 billion euros deficit just before the onset of the war in Ukraine. While this figure may seem modest, it highlights a crucial shift in the economic landscape between the EU and Russia, indicating that Europe’s strategies to reduce reliance on Russian goods are bearing fruit.

The Energy Sector: A Dramatic Transformation

The most significant change comes from the energy sector, which had previously dominated the trade balance in favor of Russia. In the second quarter of 2022, the EU’s commercial deficit in energy products reached an alarming 42.8 billion euros. However, by mid-2025, this figure saw a staggering reduction to just 4.2 billion euros, marking an impressive 90% decline. The EU’s commitment to diversifying its energy sources and reducing its vulnerability to Russian gas has led to this notable transformation.

This shift has not only improved the EU’s energy independence but has also diminished Vladimir Putin’s leverage over Europe. The concerted efforts to source energy from alternative suppliers and invest in renewable energy sources have played a vital role in this positive trend.

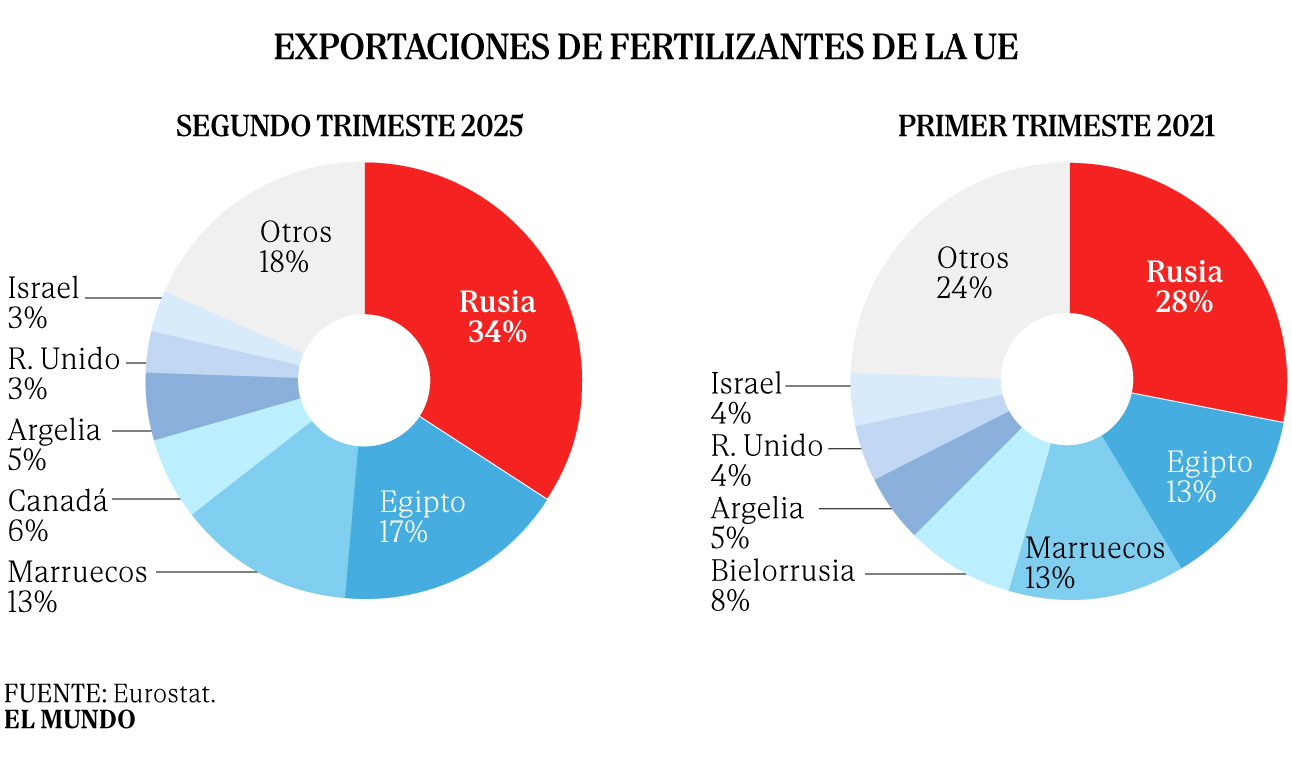

Fertilizers: A Persistent Dependence

While the energy sector showcases a notable improvement, the fertilizer market tells a different story. Fertilizers are essential for agricultural production, and this sector has maintained a steady reliance on Russian supplies. Between March 2021 and June 2025, imports of critical goods from Russia—such as natural gas, oil, and metals—were significantly reduced; however, fertilizer imports have surged from 28 billion euros to 33.7 billion euros in the same period. As a result, the EU’s share of fertilizer imports from Russia increased from 28% to 34%, making Russia the largest supplier of fertilizers to Europe.

According to McKinsey, the global fertilizer market is valued at approximately 145 billion dollars in 2023, with Russia and China being significant players. Favorable energy costs in these countries have enabled them to offer fertilizers at lower prices, leading to increased market penetration. Brussels is now taking steps to address this over-reliance.

Impact of Tariffs on Russian Fertilizers

In response to this dependency, the EU has activated tariffs on fertilizers from Russia and Belarus. The initial tariff of 40 euros per ton is set to escalate to a staggering 430 euros per ton. This move aims to minimize the entry of low-cost products into the European market, enhancing price competitiveness for local manufacturers like Fertiberia. They are hopeful that these tariffs will help limit the influx of cheap fertilizers, paving the way for a more stable market.

Reducing Dependence on Critical Minerals

In addition to fertilizers, another crucial component of trade with Russia lies in critical minerals, particularly nickel, which has extensive applications in various industries including steel, batteries, and aerospace. Recent data reveals that between the first quarter of 2021 and the second quarter of 2025, the EU’s import share of Russian nickel decreased dramatically from 41% to 15%.

In contrast, the United States and Canada have increased their imports of Russian nickel, with their shares rising by 12% and 6% respectively during the same period. This diversification strategy aligns with the EU’s objective to reduce its dependence on Russia, particularly in strategic minerals.

Conclusion

The latest data presenting a commercial surplus between the EU and Russia marks a significant milestone in their economic interaction. The EU’s concerted efforts to diversify energy sources, impose tariffs on fertilizers, and reduce import reliance on critical minerals have begun to yield positive results. While the relationship between Europe and Russia remains complex and fraught with challenges, the shifting dynamics in trade signify a proactive approach towards enhancing economic resilience and independence. The journey ahead will likely require continued vigilance and strategic planning as the geopolitical landscape evolves.

The European Union yesterday confirmed one of those rare historical events that rely on figures. In the second quarter of the year, the 27 scored their first commercial surplus with Moscow. A positive balance of 500 million euros. “Little,” says Brussels. Yes, the figure does not compensate decades of unequal relationship, but marks a turning point for the EU, which just before the war in Ukraine maintained with its neighbor a negative commercial balance of 47.4 billion.

Europe has replaced (or is close) many of the greatest units that made it vulnerable to the blackmail of Vladimir Putin. The first, the energy. The commercial deficit in favor of Moscow in energy products has gone from 42.8 billion euros in the second quarter of 2022 to 4,200 million; 90% less.

The other face of the currency are fertilizers. A sector that has monopolized fewer spotlights than gas or oil, but, indirectly, leaves the supply of basic goods for Europeans to Kremlin. Corn, citrus, wheat, vegetables … in short, the field.

Between March 2021 and June 2025, all imports from Russia of critical goods monitored by Eurostat have been significantly reduced, except for fertilizers. In that group are natural gas, nickel, oil or metal.

The EU exposure to the Russian flow of these goods ranged between 18% (metal) and 48% (natural gas) as of March 2021. At the end of last June, exposure to these supplies has cut to a fork between 2% (oil) to 19% (liquefied natural gas).

A countercurrent, fertilizer purchases have rebounded in the last four years, from 28,000 million euros to 33,700 million. Consequently, Russia not only remains the largest supplier in Europe, in addition, its share from 28% to 34% has increased. At a great distance the following suppliers are maintained: Egypt (17 %) and Morocco (13 %).

The world fertilizer market is valued at about 145,000 million dollars (2023), according to McKinsey. Russia is a great exporter, like China. Both benefit from low energy costs to offer product Low Cost. Specifically, a cheap gas, key to their production, has allowed them to take the market. Brussels has already moved to change this.

The prices of fertilizers accumulated a 15% rise in the first six months of the year, according to the World Bank. Strong demand, commercial restrictions and production shortage explain this escalation. The European Union has just activated tariffs on Russia and Belarus fertilizers. Initially, 40 euros per ton, and, later, up to 430 euros per ton. European manufacturers such as Fertiberia They expect this “to restrict product entry Low Cost to the European market ».

27 points less than Russian nickel

In commercial distancing between Europe and Russian power there is another key point, critical minerals. The twenty -seven have accelerated to replace the Russian flow of one of them, the nickel. Its versatility make this mineral a very valuable raw material for the steel industry, batteries or the aerospace sector. Between the first quarter of 2021 and the second quarter of 2025, the EU fee in nickel imports from Russia was reduced from 41 % to 15 % (a decrease of 27 percentage points), while the import fees of the United States and Canada increased during the same period in twelve and six percentage points, respectively. sanctioned, the EU began to diversify its dependence on Russia by increasing nickel imports from other countries, ”Eurostat said yesterday. In terms of cost, the twenty -seven have gone to pay more than 41,200 million euros per Russian nickel, to allocate a game of less than 15,000 million.