The Fallout of Snap’s Layoffs: A Shift in Strategy

Evan Spiegel, the CEO of Snap Inc., recently informed employees about a grim restructuring plan that entails laying off roughly 1,000 employees, which accounts for about 16% of the company’s workforce. This decision also includes the cancellation of 300 open positions awaiting hiring. Snap aims to save over $500 million annually from these cuts, although the immediate financial implications, including compensation costs ranging from $95 to $130 million, pose a considerable burden.

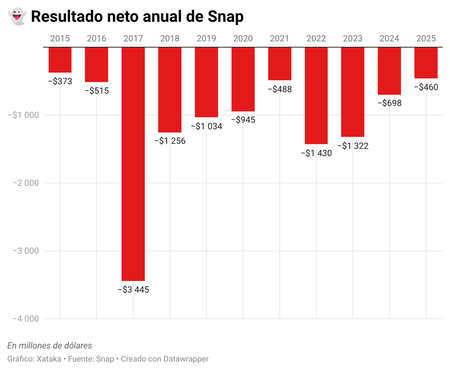

Short-Term Gains, Long-Term Issues

Interestingly, the market reacted positively to the news, with shares rising by 7%. Investors had long anticipated such layoffs, hoping they would bolster the company’s beleaguered financial standing. However, Snap’s situation is far from typical; despite its transformational role in online communication, the company has yet to establish a profitable business model. In 2025, Snap registered a loss of $460 million, continuing a trend of fiscal deficits spanning its 15-year history without a single profitable year.

The Paradox: Innovation Without Monetization

The narrative of Snap takes a curious twist beginning in 2013 with the innovation of Stories—temporary photos and videos disappearing after 24 hours. This feature became a global standard, but its original creator failed to capitalize on it. Instagram duplicated this model in 2016 and reached 100 million users in just two months, while Snap took four years to achieve the same milestone. Thus, while Snap innovated, its larger competitors quickly overtook it by leveraging superior data analytics and advertising capabilities.

The Data Gap

Unlike Meta and Google, which have extensive insights into user preferences and behaviors, Snap lacks this critical data. This discrepancy diminishes the effectiveness of its advertising, leading to lower revenues and a vicious cycle of poor performance. The implementation of Apple’s App Tracking Transparency in 2021 dealt a further blow to Snap’s advertising model, eroding profitability. While Meta also struggled, its extensive resources cushioned the impact, unlike Snap, which saw a staggering decline in stock value, sinking from $83 to around $6.

A Young Audience and Subscription Growth

Despite these challenges, Snap boasts 946 million monthly active users and a 12% year-over-year revenue growth. The platform attracts a youthful audience, making it appealing to brands in fashion and entertainment. The introduction of Snapchat+, a subscription model, has also seen promising growth.

The Road Ahead: A Focus on Sustainability

The dilemma facing Snap is not easily resolved by mere cost-cutting. While this approach will enhance margins, monetizing a platform with a predominantly young audience remains a significant hurdle, especially when competitors possess far more resources. Additionally, activist investor Irenic Capital Management owns 2.5% of Snap and has been pushing for similar cost reductions.

Strategic Refocus

Looking to the future, Spiegel has outlined a strategic shift towards consolidating investments in areas with proven monetization potential. This may involve withdrawing from challenging markets—such as Spain—while concentrating on more lucrative regions like the United States or the United Kingdom, favoring sustainability over aggressive growth.

Snap has been grappling with challenges for 15 years, struggling to find a viable equation for profitability. These layoffs serve as a temporary solution, affording the company some breathing room to refine its strategy for the future.

Featured image | Shutter Speed

In Xataka | Snapchat introduced its own version of ChatGPT in its app. Nothing has gone, nothing good.