In an environment where volatility remains a constant, high-quality European corporate debt emerges as a rational refuge. The combination of a European Central Bank with a margin of action, differential at low levels, and still attractive profitability compared to its historical average, coupled with inflation under control in the eurozone, creates a favorable setting for conservative investors, which is difficult to ignore.

The recent correction of interest rates has re-established attractiveness in emissions that barely offered profitability a year ago, now exceeding 3% at expiration. In many instances, these corporate debts come with additional premiums against similar sovereign bonds. In this scenario, it’s not just about seeking performance, but about avoiding unnecessary shocks: European credit offers a balanced risk-return profile that increasingly captures the interest of large international managers.

Additionally, the more disciplined fiscal context in Europe, along with a reduced reliance on short-term financing by companies, has reinforced the perception of solidity of European credit compared to its American counterparts. Given electoral uncertainty in the US and ongoing global geopolitical noise, the institutional stability of the eurozone serves as a crucial anchor for the most prudent investors. Today, European corporate debt stands out as one of the few assets that harmonizes profitability, liquidity, and resilience amidst uncertain times.

Long American Bonds: Refuge or Undercover Risk?

For decades, long-term US Treasury bonds were considered the ultimate refuge asset. However, in today’s landscape, that once-unquestioned reputation is beginning to appear more like an illusion than a reality. The challenges are no longer limited to the high duration and price sensitivity to shifts in profitability but also encompass the structural context of an economy reliant on artificially low interest rates, limitless stimuli, and escalating public debt without political checks. Instead of being a protective measure, these bonds are increasingly viewed as one of the main risk vectors within conservative portfolios.

Monetary policies marked by extremes (zero nominal rates, financial repression, curve control, and the nationalization of central bank balances) have transformed what was once deemed a safe asset into one which may result in significant market scares. Investors who buy Treasury Bonds with maturity spans of 20 or 30 years are accepting yields that may not adequately compensate for inflation risks. Furthermore, for European investors, the potential evolution of the currency introduces an additional layer of risk.

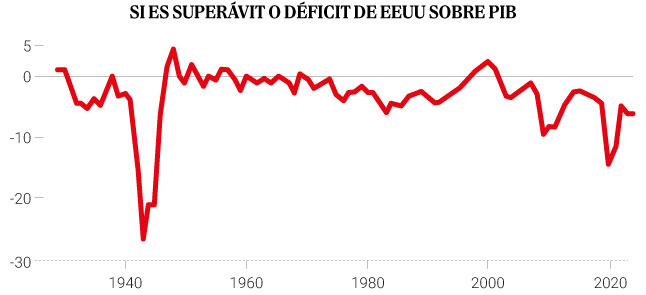

Further exacerbating the situation are fiscal risks: the United States has abandoned any semblance of budget discipline. With a pattern of excessive spending, unchecked borrowing, and monetary strategies that could potentially lead to structural inflation, a loss of confidence, and possible currency wars, the landscape for long-term US bonds darkens. If market participants pull back from buying these securities, the Federal Reserve may be forced to step in and purchase everything again, but such actions won’t protect the investor; they merely prolong market distortions.

This creates a precarious paradox: an asset that continues to be considered a safe haven while simultaneously exhibiting warning signs reflective of an intervened economy, indicating that investors should tread carefully.

*Rafael Ciruelos is a partner and director of Diaphanum Funds Selection.