Updated

On July 12, President Trump sent a letter to the EU proposing a 30% tariff on products entering the United States. The August 1 deadline leaves some room for negotiations, but time is undeniably limited. If these tariffs are implemented, the negotiations will likely continue, aiming for a resolution sooner rather than later. However, the impact of these tariffs will vary across different sectors, necessitating preparedness. Generally, the services sector tends to be less affected compared to manufacturing . The consequent implications will be more pronounced in sectors heavily reliant on domestic suppliers. Thus, it’s important to identify potential winners and losers in this evolving economic landscape.

Starting with consumer goods , luxury companies are likely to be the least affected. Their high margins and robust pricing power make them less vulnerable. However, they may face indirect effects such as changing consumer sentiment . Another sector that has been under scrutiny is pharmaceuticals , which currently avoid tariffs, but face a looming threat . According to President Trump, these tariffs may be introduced within 1 to 1.5 years , ostensibly to incentivize large pharmaceuticals to relocate production to the U.S. The uncertainty caused by these rumors has led many investors to withdraw from these companies, reflecting a sentiment that the commercial risk is already factored into current valuations, albeit some volatility remains likely.

The industrial sector , a key priority for major fiscal projects in Europe, could face challenges as well. However, it typically boasts more localized production and higher pricing power. Additionally, many companies in this sector have established tariffs and enjoy significant market leverage. Consequently, the major risk for European industrial firms, particularly in the automotive sector, revolves around diminishing global economic forecasts, which could hinder customer decision-making processes and weaken order reception . Industries that are linked to secular growth factors like electrification are expected to be better positioned against these uncertainties. In summary, while the final stance on tariffs remains uncertain, it’s evident that many firms are preparing for the worst-case scenario.

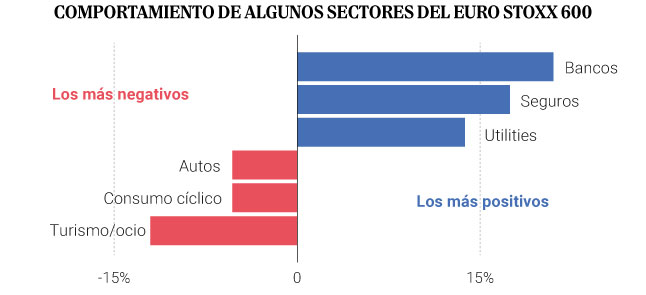

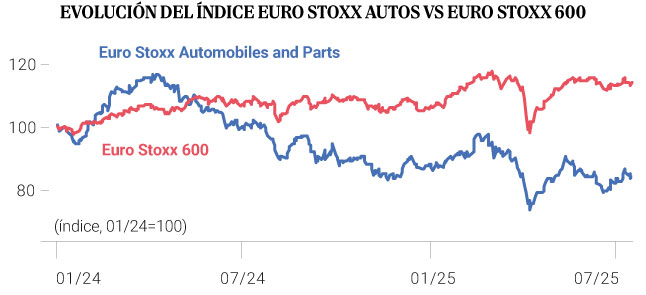

Bad Times for the European Automobile Industry

The European automobile industry has been navigating a crisis even before Trump’s recent announcements. Factors such as supply chain disruptions , slowing electric vehicle adoption rates in both the U.S. and Europe due to reduced government subsidies, and intensifying competition from China have compelled many companies to reassess their profit projections. The prospect of additional tariffs adds yet another layer of risk for the European automotive sector. Notably, the industry has developed a globally diversified production infrastructure with supply chains spanning multiple countries.

Within this industry, companies producing mid-range cars entirely in Europe may become the most impacted by these tariffs. In contrast, firms with significant production in the U.S. or focusing on the luxury segment—who can pass on tariff-related costs to consumers—are less likely to suffer immediate financial repercussions. Overall, while there are optimistic forecasts for a cyclical recovery in Europe over the next two years, this positive outlook might not be enough to alleviate the pressures on car manufacturers currently undergoing substantial restructuring efforts.

*Rosa Duce is Chief Investment Officer of Deutsche Bank in Spain.

General News – 2