China’s Semiconductor Ambitions: The Race Against Taiwan

China is on the brink of a semiconductor revolution, with a recent report from the Yole Group indicating that the nation will likely surpass Taiwan in semiconductor production capacity by 2030. This shift is driven by strategic investments and advancements in technology, showcasing China’s ambition to dominate the global semiconductor market. While quantity may be on China’s side, questions linger over the quality of the chips produced.

Understanding the Chinese-Taiwan Tension

The dynamic between China and Taiwan is complex and strained, particularly in the realm of technology and semiconductors. Taiwan’s TSMC (Taiwan Semiconductor Manufacturing Company) stands as a powerhouse in the semiconductor industry, renowned for producing high-quality chips that are pivotal for various tech sectors. Unlike China, Taiwan is not subject to significant manufacturing restrictions, which fortifies its current lead. However, China’s response has been aggressive, with substantial investments in domestic semiconductor companies and foundries, allowing them to make significant strides.

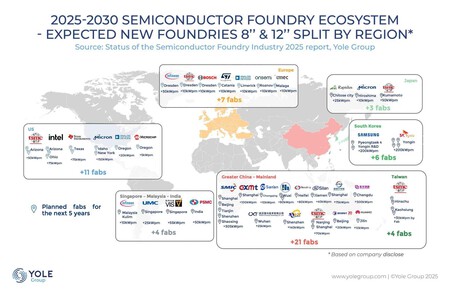

Production Capacity: The Current Landscape

According to the recent study, it’s projected that semiconductor production capacity in Chinese plants will account for 30% of the global market by the end of the decade, up from 21% in 2024. Currently, Taiwan holds a 23% share, with China closely following at 21%. Other leading nations in the semiconductor race include South Korea (19%), Japan (13%), and the United States (10%). This data reveals not just a significant growth trajectory for China but also the potential for a dramatic reshaping of the semiconductor industry landscape.

The Role of the ‘Big Fund’

For years, Beijing has aimed to become a self-sufficient player in the semiconductor field. To achieve this goal, they established the Integrated Circuit Industry Investment Fund, commonly known as the “Big Fund.” This initiative has facilitated financial backing for key players in the Chinese semiconductor industry, most notably SMIC (Semiconductor Manufacturing International Corporation) and Hua Hong Semiconductor. The funding has proven instrumental in boosting the capabilities of these companies, making significant advancements possible.

Evolution of Chinese Semiconductor Manufacturers

The progress of domestic semiconductor manufacturers in China is noteworthy. They are prioritizing investments in expanding their capabilities to produce chips tailored for sectors such as automotive and artificial intelligence (AI). This evolution paints an optimistic picture for the Chinese semiconductor industry, although many hurdles remain, particularly concerning cutting-edge technologies.

Quality Versus Quantity

While Chinese manufacturers excel in boosting production volumes, they face significant challenges regarding quality. The semiconductor plants in mainland China predominantly utilize older photolithography technologies, operating between 8 to 45 nanometers. This technology is adequate for manufacturing chips for sectors like automotive and IoT devices but falls short for advanced applications, particularly in AI, where TSMC continues to excel.

Challenges for China’s Semiconductor Giants

SMIC, the leading semiconductor manufacturer in China, has encountered hurdles in transitioning to a 5 nanometer photolithographic process. This technology leap is proving difficult, and issues have emerged with their existing 7 nanometer nodes, which have shown underwhelming performance. These challenges could hinder China’s ambitious goals in semiconductor production, creating a bottleneck as it attempts to scale up its technological capabilities.

Global Competition: Taiwan and South Korea

While China strives for semiconductor self-sufficiency, rivals such as TSMC and Samsung are rapidly advancing. TSMC is on target to start mass production of 2 nanometer chips later this year, while Samsung projects a similar milestone by 2026. Taiwan is also innovating its A14 lithography process, aiming for large-scale production by 2028. This relentless pace of innovation highlights the highly competitive nature of the semiconductor market.

In conclusion, China’s aspiration to surpass Taiwan in semiconductor production capacity reflects significant progression but does not come without challenges. The investment in producing more semiconductors is substantial, yet the ability to manufacture cutting-edge chips remains a threat to their overarching goals. As global competitors accelerate their manufacturing capabilities, the landscape of the semiconductor industry will continue to evolve, closely watched by both technological leaders and policymakers.